Organization and Operation of Internal Audit

Internal Audit Organization

The Company has an auditing office, which is responsible for the Company's auditing work. The staffing is two to three people, who belong to the board of directors. Before the end of January every year, the basic information of the auditors and the education and training courses they have received will be reported online, and the internal auditors will be checked at any time whether they meet the qualification and full-time requirements. In addition, the appointment and dismissal of the Company's audit supervisor must be approved by the Audit Committee and the Board of Directors, and must be reported online to the competent authority for reference before the tenth day of the month following the approval by the Board of Directors.

The appointment, dismissal, evaluation, and salary of the Company's internal auditors are in accordance with the relevant regulations of the Company's internal control procedures, and are handled by the approval method signed by the audit supervisor and reported to the chairperson.

Internal Audit Operations

-

Internal audit scope

Account review, Inspection of property, Operation review, Procurement and contract auditing, Budget audit, Other matters

-

Internal audit implementation procedures

Preparatory work before the audit, On-site inspection, Analytical research, Audit report summary, Lack of improvement tracking

-

Execution of internal audit work

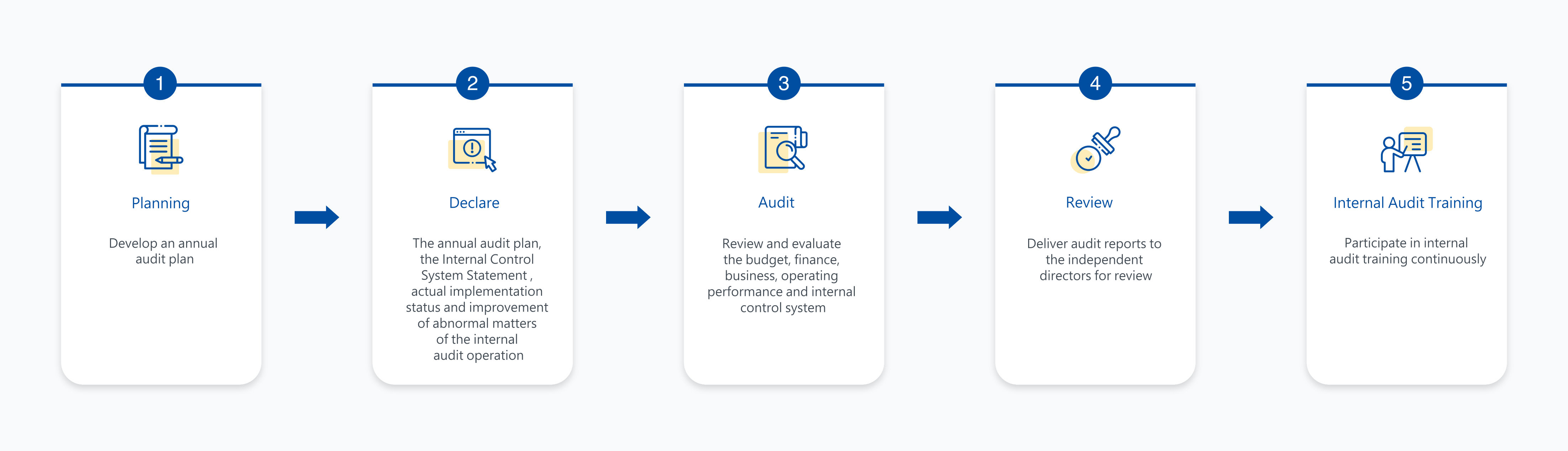

- An annual review plan for internal audit operations should be drawn up to implement the audit work accordingly.

- The company shall report the audit plan for the next year before the end of each accounting year; within two months after the end of each accounting year, report the implementation status of the annual audit plan for the previous year; five months after the end of each accounting year within the report, report the improvement of deficiencies in the internal control system and abnormal matters found in the internal audit of the previous year. The declaration method is to declare online through the Internet information system according to the prescribed format for future reference.

- Internal auditors should review and evaluate the Company's budget, finance, business, operating performance and internal control system based on the annual audit plan, and attach working papers and random inspection data, etc., and prepare an audit report for review. Audit reports, working papers and related materials should be kept for at least five years.

- The audit report prepared in accordance with the above provisions shall be delivered to the Company's independent directors for review before the end of the month following the completion of the audit project. In addition to the audit report, the annual audit plan, actual implementation status and improvement of abnormal matters of the internal audit operation should be reported to each independent director or the audit committee.

- Internal auditors should continue to participate in internal audit training organized by professional institutions or the company itself to improve audit quality and capabilities.